Friday, November 12, 2010

The collapse of Europe ? If you believe so, short the Euro.

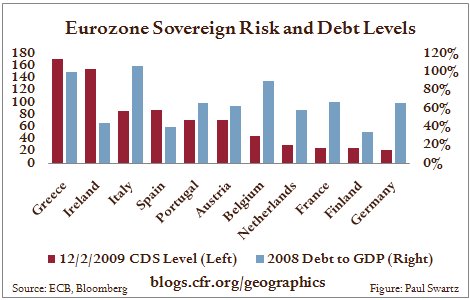

800% of GDP in real debt including future obligations.

by StFerdIII

The 800% or more of GDP which is Europe's real debt cannot be avoided, watered-down, sold to someone else; or buried in a big hole somewhere and forgotten. The nirvana of European socialism, guarantees, compassionate rhetoric and multi-cult love is bankrupt. Everyone must know this. One of the energizing impulses of ever-closer-union and the establishment of the 1992 EU zone; was the spectre of financial and economic impoverishment.

The whole political point of the EU was to use more dynamic economies such as Germany and England to fund the rest – especially voters, farmers, and union workers in France, Spain, Italy and Greece. But when you rely on one group of statist entities like Germany and England to finance more constricted and benighted socialist creations like Italy or Greece, the game is a loser from the start. A poor man with 2 eyes, cannot shuffle his money over the poor man with one eye. In the end you still have 3 eyes and 2 beggars. The day of reckoning, put off by EU 1992 and its expansion, was delayed but not nullified.

The more aggressive of the EU nay-sayers sound a lot like John Taylor, a well-known trader and strategist. Mr. Taylor is certain that the Euro will collapse as the debt problems of the socialist construct consumes EU states. He believes the recession will extend, imploding the economies of Europe and the US:

Jean-Claude Trichet caught the spirit of the situation today in Seoul when he said that “it is absolutely necessary to change the governance of Europe” and called for moving “as far as possible in the direction of an economic and budgetary quasi-federation.” I only disagree with part of one word, ‘quasi,‘ as Europe must move to a full economic federation if the euro is to survive. With 16 countries using the euro and Estonia on the way, the odds of moving there is currently lower than infinitesimal. Things will change after the approaching horrible economic and political catastrophes that will wrack some of these economies and societies. Unfortunately nothing will happen before the current situation gets unbearable – this is the way of democratic politics. As all the leaders are still working toward the same goals, and no one has stepped forward express the inchoate fears of the European populace, this should take years. By the start of next year the Eurozone will enter a recession that will test the current leadership. The euro, which has been perceived as if it were a German mark, has already topped and will decline until it is priced like an Italian lira in the next few months. With Europe and the US in recession next year, commodity prices will drop again and global growth will suffer despite the outperformance of domestic Asian economies. With the policy stresses, and the risk of significant errors in judgment, international strife becomes more likely as well.

The well-worn argument is that declining economic fortunes lead to war. This is not supported by historical fact. It is highly unlikely that Europe will dissolve into a civil war, or that a war with Asia or some other non-EU power will occur. The Europeans don't have a military to start with, neither do they have a culture predisposed to aggression. 60 years of cultural Marxist theology tends to neuter most instincts which trend to the aggressive. The most likely scenario is that the Euro first unravels as nation states blame 'the Union' for their political-economic ills. When the Euro is dissolved the EU itself will be reformed into a free trade-only era. Brussels will no longer hold political sway – and that will be a huge benefit for Europe and the world.

Some feel however that the collapse of Europe is perhaps over-stated. Events are more 'nuanced' than a general sovereign-banking debt implosion across the Continent. The supposedly-conservative Wall Street Journal maintains that as far as certain countries like Ireland are concerned, things are much better than the media reports. According to the WSJ editorial board the only problem with Ireland is that its banking sector will require 50% or more of GDP in bailouts. This financial sector bankruptcy is 'quite different' than the state debt problems of say Greece or Hungary. Or is it? In Ireland's case the economic havoc was wrought by government using the housing and home-finance markets as political tools. Whether the state goes bankrupt from a financial implosion, or the noxious allures of statism and socialism matters not.

The WSJ is very likely, quite wrong. Ireland is teats up. So too are most EU states. A Continent in which toilet seat sizes are regulated, and taxes take over 50% of gross income, will one day either face disintegration and rebellion, or a rude descent into insolvency. Short the Euro, buy the EUO ETF.